The Dollar Dump II?

Or Confirmation Bias?

Today, the focus is to examine the similarities and differences between the economic war President Trump launched last year and the military war he launched in March.

The objective is to attempt to answer these two questions:

What is the likely path of the US dollar?

Given that path, what portfolio adjustment makes sense?

A little history of the relative performance of the US and foreign stock markets may help us find the answers.

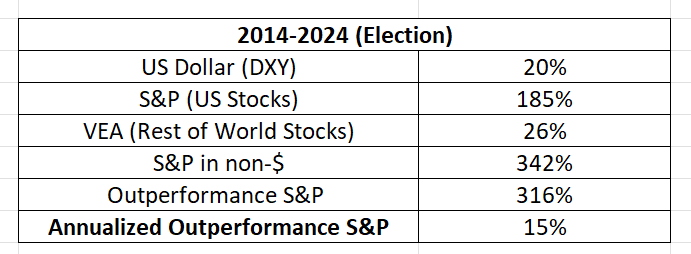

The Glorious Decade of the Dollar

For the decade preceding President Trump’s election, foreign investors had a field day investing in the United States. Consider the returns of three asset classes:

The US Dollar (DXY Index)

US Stocks (S&P Index)

“Rest of World” Stocks (ETF VEA)

The foreign investor who sold his or her home currency to buy US dollars, then used those dollars to buy the S&P, earned three times more than the foreign investor who invested in his or her home country, or 15% per year of outperformance.

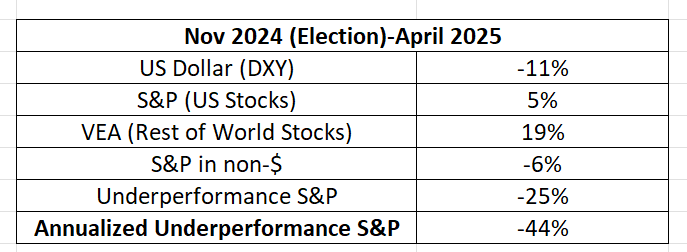

Dollar Dump I

Then Donald Trump was elected. The flavor of asset allocation started to change, and foreigners invested in US stocks started to get a bad taste in their mouths. Not only did the dollar fall, but Rest of World stocks took off relative to the S&P.

Here is the period from Election Day to Liberation Day, when Trump effectively declared economic war on the rest of the world, raising tariff rates on average by 400%.

This is the “Dollar Dump I.”

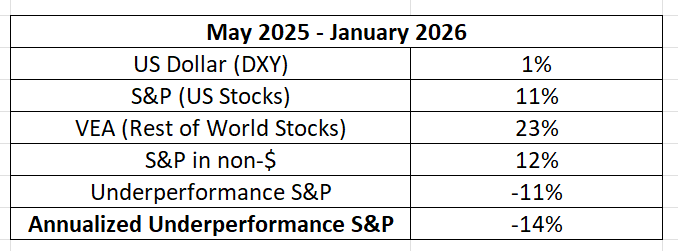

Then the dollar stagnated until the drums of war started to beat at the end of January this year. In this period, Rest of World equities continued to run circles around the S&P. The song remained the same.

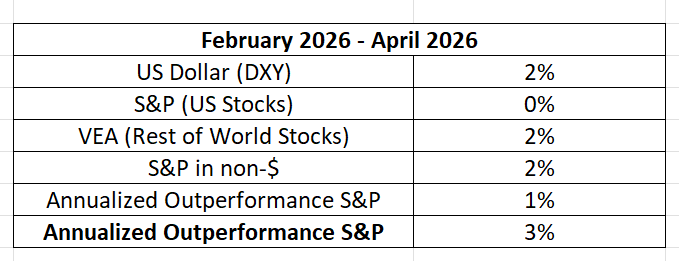

Wartime Dollar Strength

Dear reader, consider how these three asset classes have performed since Trump declared another war with macroeconomic implications - a military one against Iran:

Has the market flavor reversed once again to favor the dollar?

Is the greenback back?

My answer (guess): No.

The AI Angle

One reason the S&P underperformed the Rest of World is that market leadership in the United States moved from large-cap technology “Magnificent 7” companies to non-tech, “asset-heavy” companies like those in the energy, materials, and industrials sectors.

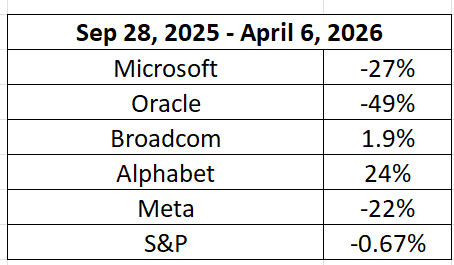

Back in this September post, I (poetically) transformed the Magnificent 7 into the “Sexy Six,” removing Tesla, Apple, and Amazon, and adding Broadcom and Oracle, who had become AI heavyweights.

This final table illustrates the new market leadership, with the Sexy Six becoming the “Frigid Five,” while the S&P remained stable. Non-AI sectors compensated for the AI pain.

What have we learned?

Net money flowed out of tech into non-tech

Net money flowed out of the US stocks into Rest of World stocks

Net money flowed out of the US dollar

Two primary narratives explain these movements:

First, the flight from tech was a result of the market’s reassessment that the billions of dollars earmarked for AI investment may not necessarily have a satisfactory return on investment. The market isn’t asserting that the investments won’t pay off; it has simply assigned a higher risk premium due to the lack of visibility.

Microsoft is the poster child of this phenomenon.

In September 2025, the forward P/E was approximately 33.0.

Today, the forward P/E is 21.

Why is Microsoft so soft? First, much of its business is producing and selling software. With agentic AI improving exponentially (see the post “Portfolio Intelligence”), the whole software sector has been slaughtered.

Second, Microsoft owns 27% of OpenAI, the company that developed ChatGPT. OpenAI, along with SpaceX and Anthropic, may be coming to market with Initial Public Offerings (IPOs). Considered together, the market will need to absorb literally trillions of dollars of new funding - both equity and debt.

For the markets to “make room” to digest this supply, assets must have a higher risk premium (their price goes lower), and that supply/demand imbalance makes investments in the US dollar less attractive.

But AI risk alone doesn't fully explain the dollar's weakness. The second narrative brings us back to where we started — and it has nothing to do with Silicon Valley

The second narrative circles back to the beginning of this post.

Could the Iran war set off a round of dollar devaluation like the trade war did last year?

What do the two wars have in common?

Disruption of the established world order

Degradation of traditional alliances

Deleterious impact on economic growth and inflation

What do the two NOT have in common?

Fiscal flow.

Tariffs, even after the Supreme Court struck some down, bring in revenue for the Federal Government. Tariffs decrease the deficit. It is hard to pin down the exact tariff revenue the federal government will collect this year, but $100-$200 billion is a good ballpark guess.

The Iran War? It increases the deficit. Some estimate that the US has already spent upwards of $40 billion, and that if the war lasts months, the price tag could jump to $200 billion.

Although visibility is not perfect, it seems safe to say that the war’s net fiscal hit versus tariffs is in the neighborhood of $400 billion. That is 1.3% of GDP.

For those reasons - higher AI risk, heightened geopolitical instability, and higher deficits - the likely path is for the dollar to resume its downward trend, and for Rest of World stocks to resume outperforming the S&P.

My own portfolio allocates roughly one-third of non-cash assets to currencies other than the US dollar.

The Other Side of the Dollar Bill

Pundits pronounce, analysts analyze. And your faithful analyst acknowledges that events are unpredictable and alternative scenarios exist that are entirely plausible.

Here are three counterarguments to the Dollar Dump II thesis:

AI productivity boost is more immediate than expected, expanding US profit margins faster than in the Rest of World, and thereby attracting foreign capital.

The war ends quickly, and damage to the budget is contained.

The US brings about Iranian regime change (or modification of the present regime’s behavior), giving Trump a resounding military, strategic, political, and economic victory.

These scenarios are all highly positive for the dollar and S&P.

Confirmation Bias

One of the chief challenges in trading, and in life, is understanding one’s own biases. I am not a fan of President Trump politically or personally, and did not see the “imminent threat” posed by Iran to US security.

It is eminently possible that the investment thesis of dollar avoidance is derived from this predisposition.

I hope my analysis is not biased, and I think it is not, but you have been forewarned.

Remember, this newsletter aims to provide investment inspiration, and not investment advice. Please do your own homework.

If you liked this post, please leave a like on the website HERE.

Thank you kindly.

Personally, I'm with you on the dollar weakness predisposition. I've also consulted with the technical analysis gods, and they seem to agree.. ;)