Two Poetic Masterpieces

Stocks and Bonds, Romance and Revulsion

[For best visualization, read on the website here]

Two poetic masterpieces begin with two very different descriptions of the month of April.

Geoffrey Chaucer’s The Canterbury Tales, written ca. 1390, starts like this:

In the original Middle English:

“Whan that Aprille with his shoures soute,

The droghte of March hath perced to the roote

And bathed every veyne in swich licour

Of which vertu engenedred is the four…”

In Modern English:

“When April with its sweet showers

has pierced the drought of March to the root,

and bathed every plant vein in such liquid

that gives the power to grow the flower…”

For Chaucer, April is celebratory and optimistic. It is a time of renewal, rebirth, and awakening.

Chaucer could have been describing April of 2026 for stock market investors.

The second masterpiece is by T.S. Eliot, who turned Chaucer’s romanticism on its head in the opening line of his nihilistic 1922 poem, The Waste Land.

“April is the cruellest month, breeding

Lilacs out of the dead land, mixing

Memory and desire, stirrring

Dull roots with spring rain…”

For Eliot, April is bleak and despairing. He describes a world that is barren and spiritually dead.

Eliot could have been describing April of 2026 for bond market investors.

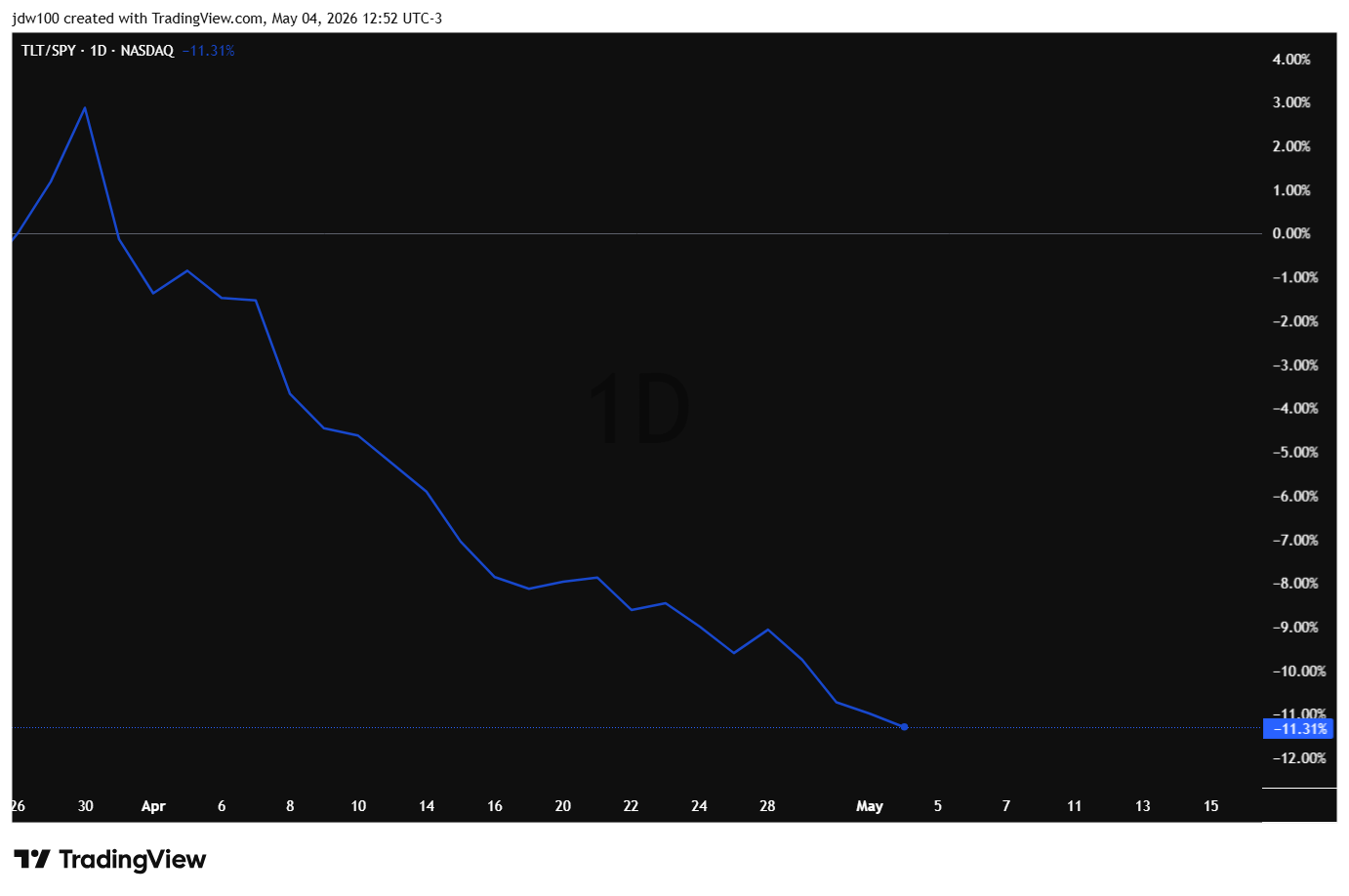

Let’s first see what happened in March. The SPY (the S&P ETF) fell 5.20%, and TLT (the long-duration Treasury bond ETF) fell 5.4%. That surprised no one. Soaring oil prices would not only force central banks to raise interest rates (hurting bonds) but would also sap economic demand and therefore lower corporate profits (hurting stocks).

But that dynamic changed radically in April.

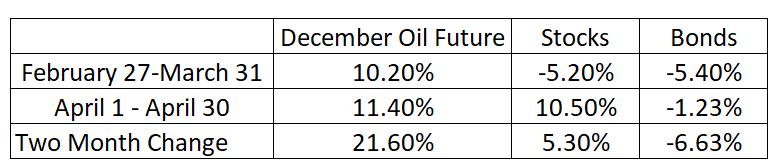

This is the chart of the ratio TLT/SPY in April. Bonds underperformed stocks by 11.3%!

To summarize:

Before attempting to diagnose bonds’ April sickness and psychoanalyze stocks’ April euphoria, if you will permit me, I would like to tell a story from my trading past.

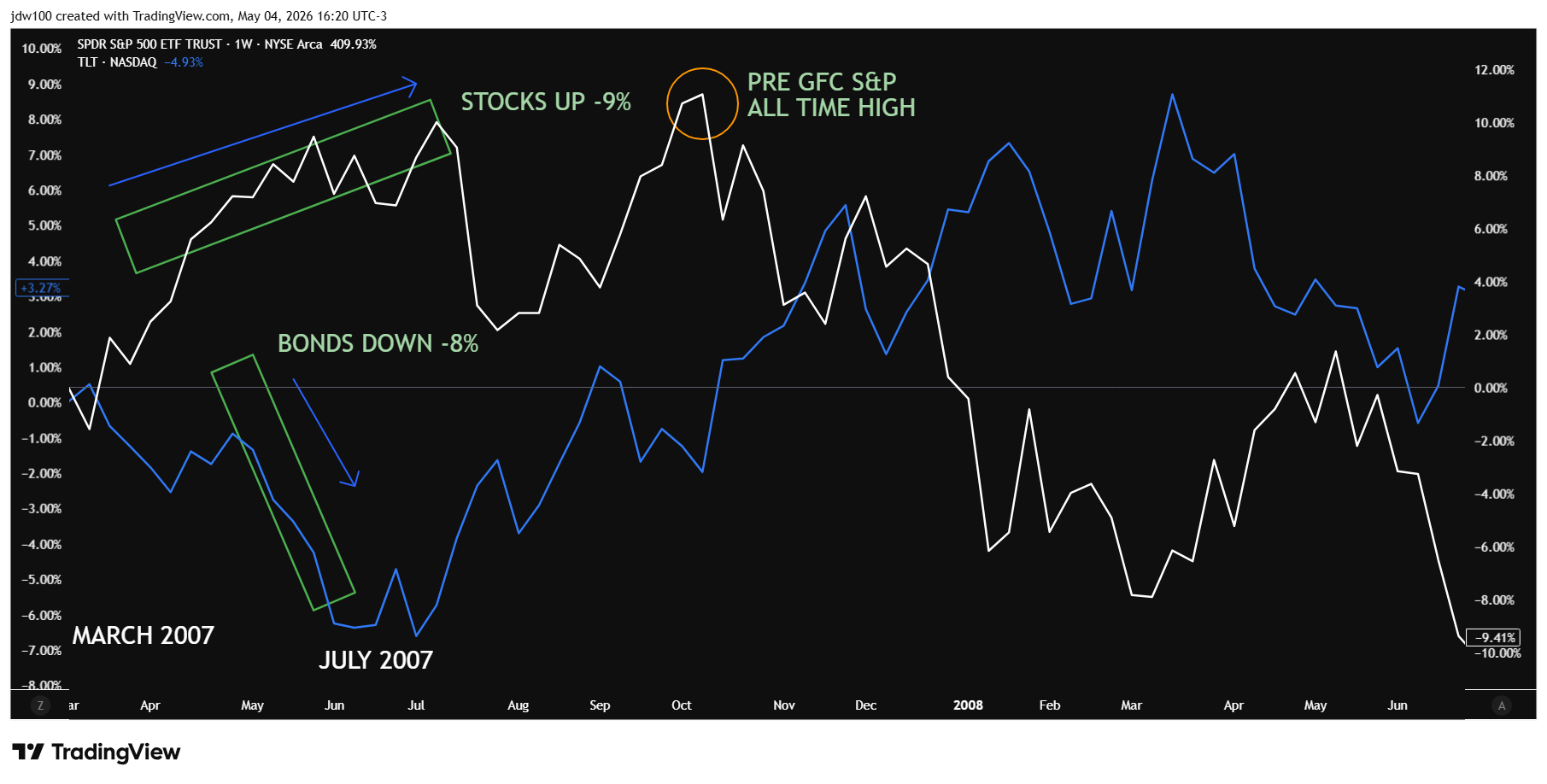

I was a portfolio manager for a hedge fund based in London in March 2007.

We were attuned early to the developing weakness in the subprime mortgage market and believed that other types of credit could be contaminated, pushing stock prices lower. We went short the S&P.

From March to July, TLT sold off 8%, interestingly, partially on the back of higher oil prices. But that gave us another reason to be short - higher rates couldn’t be good for stocks, we reasoned.

The market had other thoughts. In those four months, the S&P traded 9% higher, oblivious to any signs of the coming credit crisis or higher interest rates.

This graphic shows the blow-by-blow evolution of this stock/bonds divergence. in 2007 and 2008.

[Stocks are the white line; bonds are the blue line].

Sometime in September, we threw in the towel and tragically covered the S&P short. I say tragically because it turned out that the high in the market came in October, after which it fell 50% over the next 15 months. Meanwhile, TLT rallied 15%.

Coulda, woulda, shoulda.

Now that you know this war story will never make it into Trading Wizards 8, let me attempt to explain its relevance.

The divergence between stocks and bonds we witnessed this April reminds me of the one back in 2007.

Perhaps you are thinking, “What a useless comparison, today’s Middle East crisis is not the same thing as the subprime crisis.”

Of course, it’s different. That doesn’t mean that a subjective comparison is not useful. And in this case, the comparison is as much intuitive as subjective.

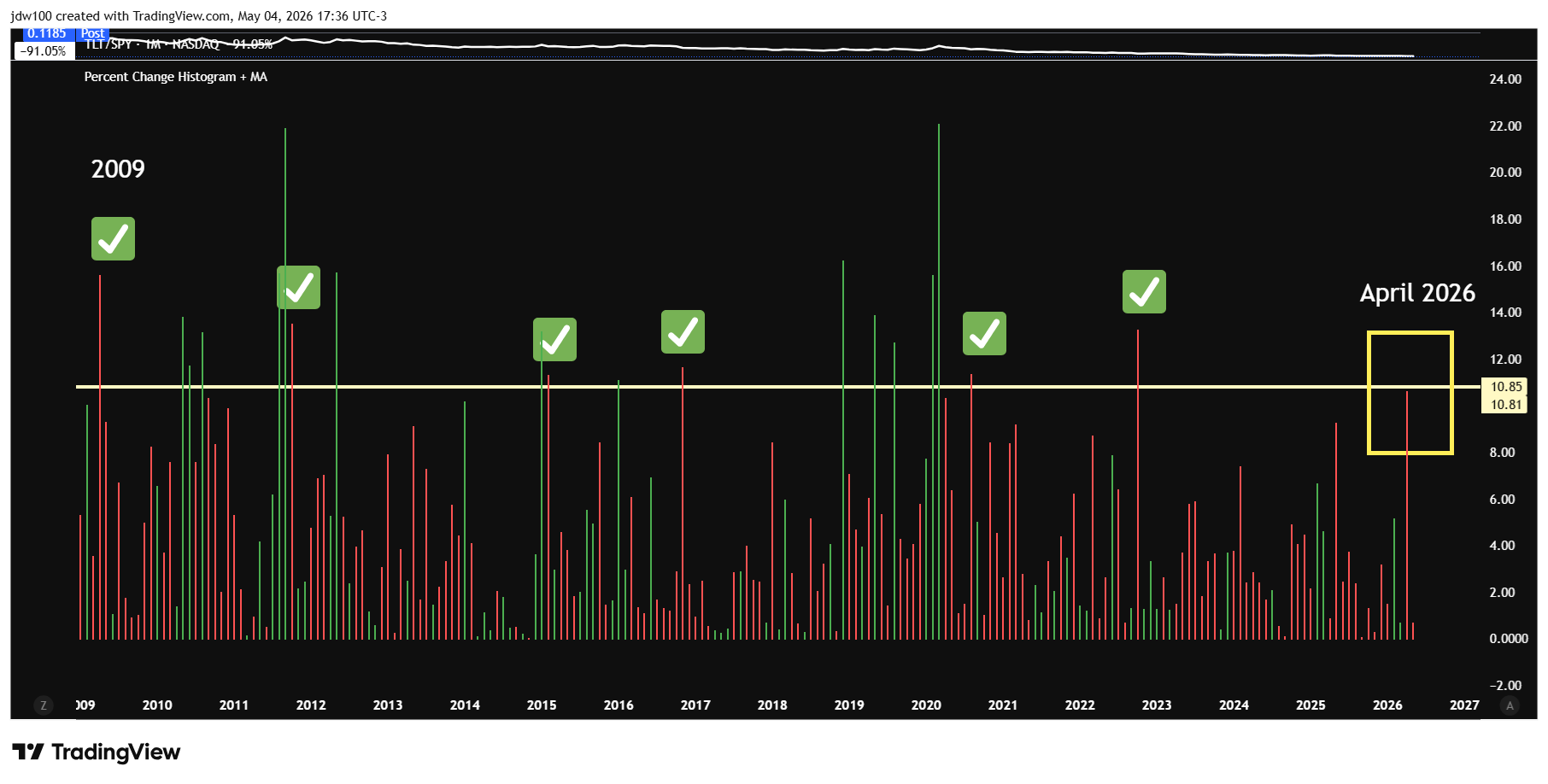

But let’s be objective first: how many times since the GFC have stocks outperformed bonds in a month as much as they did in April? Take a look at this chart I ran on TradingView*:

In the 204 months since the market bottomed in 2009, there have been only six instances when stocks outperformed bonds more than they did last month.

I am not crazy. This signifies something.

Through the rearview mirror, the stock/bond distortion in the spring of 2007 was one of many indicators that markets had become irrational.

Are markets irrational today? It sure feels that way to me subjectively and intuitively.

What is objectively true is that bonds are much more attractive to stocks than they were 32 days ago.

If you want me to tell you to buy bonds and sell stocks, then you will be disappointed. The wolf of wall street’s objective is to provide investment inspiration, not investment advice.

I can’t think of a better way to wrap it up here than by invoking another classic line from The Waste Land, followed by my own adaptation.

Eliot wrote:

“This is the way the world ends

Not with a bang but a whimper.”

I’d say:

“This is the way this post ends

Not with a bond but a whimper!”

[If you enjoyed this feature article, please leave a like on the website here.]

*TradingView indicator utilized “Percent Change Histogram.”

Cool tradingview chart (last one)! Definitely pretty omnious times...

Thanks for the post!