Bond Bust

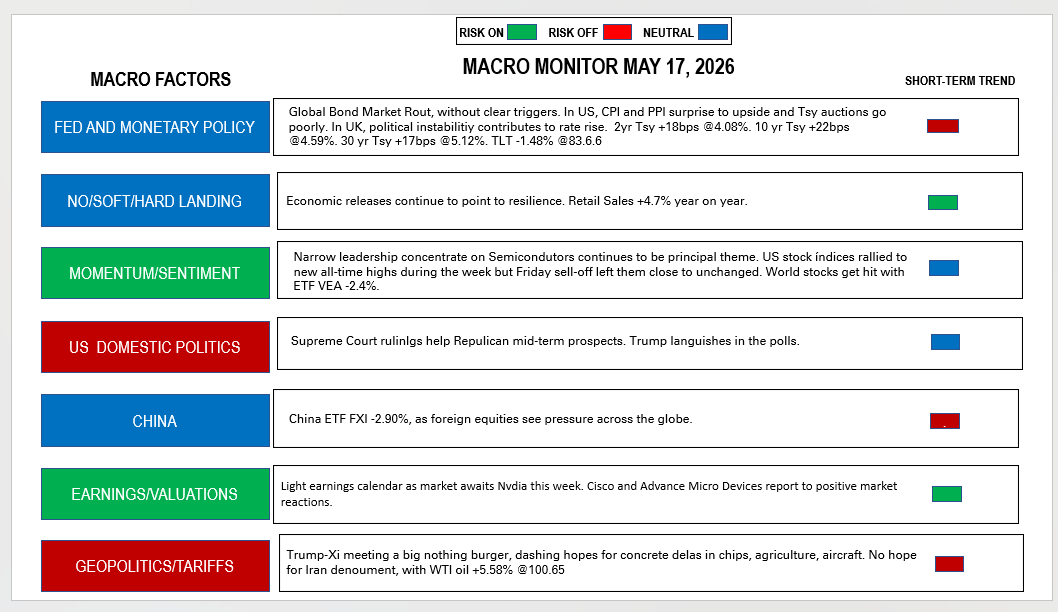

Macro Monitor, May 17, 2026

The Past Week

No reason to be long-winded. This is what happened last week:

In other words, the 2026 bond market bust is reaching a crescendo.

The carnage in bond prices and rise in yields have been global.

Thirty-year Japanese Government Bonds (JGBs) closed above 4% for the first time since they were first issued in 1999.

United Kingdom Government Bonds (gilts) took an even greater hit. Intensified by instability in Prime Minister Keir Starmer’s government, yields in the long-end soared 25 basis points.

This daily chart of ten-year gilt illustrates the damage done since February.

The UK hasn’t seen yields this high since 2008.

It is difficult to pinpoint an exact trigger for this week’s sell-off. But here are three sources of bond market discontent:

Inflation Readings

Inflation readings across countries have put central banks in a corner. In the US, for example, April CPI (retail inflation) registered 3.8%, miles away from the Fed’s 2% target. In Japan, wholesale inflation came in at 4.9%, diverging wildly from economists’ expectations of 3.0%.

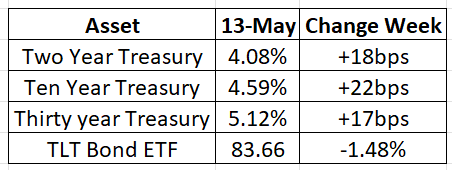

Bond Supply

Last week, auctions of three, ten, and thirty-year US Treasuries went poorly.

As the Iran conflict drags on, markets are increasingly worried about the need for more government financing. Trump’s request to Congress to authorize $1.5 trillion for 2027 defense (“war”?) spending has been a clarion call to the bond vigilantes. That would represent a 40% increase from 2026.

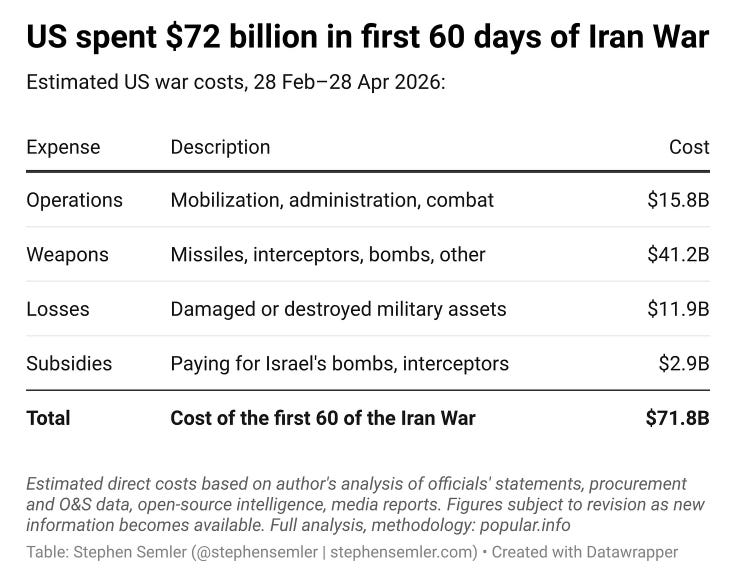

The Pentagon’s claim that the cost of the war has been $25 billion is not credible. Stephen Semler, a journalist who co-founded the Security Policy Reform Institute, estimated in a Substack post last week that the war had cost nearly $72 billion in its first 60 days.

Oil Prices

West Texas Intermediate oil (WTI) rose 5% to just over $100/barrel. Brent oil, which supplies Europe, rose to $109/barrel.

The CEO of Saudi Aramco, the world’s largest oil producer, said this in last week’s investor call:

“The longer the supply disruptions continue, even for another few more weeks, it is going to take much longer time for oil market to rebalance and stabilize.

“It could drag on to 2027 to return to normal levels. All it takes for that to happen is another shutdown if you take it from the 5th of May, another 6 to 8 weeks, middle of June to drag it into 2027.”

Aramco’s words of warning are echoed in the markets. Recall that WTI oil was priced below $60/barrel at the turn of the year. Since then, the spot market has risen more than 60%. But looking at the futures curve, December 2026 delivery is trading at $83/barrel, a 35% increase year on year.

President Trump’s insistence that oil prices will tank once the Strait is reopened is more political posturing than economic forecasting. In the medium term, countries will need to restock the strategic reserves they released to compensate for reduced supply from the Middle East. Longer-term, oil, natural gas, and fertilizers that pass through the Strait of Hormuz will carry a geopolitical risk premium that the markets did not require before the war.

Finally, any hope that Trump could convince China’s President Xi to pressure Iran into more serious negotiations was dashed as their summit resulted in no concrete agreements.

How did other asset classes perform during this bond market bust?

Gold and foreign equities fell hard with bond prices, while the dollar rose globally. U.S. equities, led by persistent strength in AI companies, were again the standout asset class. Despite the ancillary market turbulence, the S&P was unchanged on the week.

The Coming Week

The key to the coming week may be technical. The S&P, as discussed last week in the post “Bubblicious,” has been on a tear that is typical of a bubble. Whether the bubble is in its middle stages or close to popping is unknown to anyone. However, Friday’s price action was weak, with the index 1.4% and closing at the week’s lows.

Here is the weekly chart of the S&P:

Note the “wick” of the last candle. The height of the “wick” - the distance from the week’s intraweek low to its intraweek high - is long relative to the “body”, the green rectangle formed by the week’s opening and closing prices. That means that higher prices were rejected - and that movement came quickly on Friday.

Equities are not currently priced for higher interest rates. If bonds continue to sell off, this observer doesn’t see much upside for the S&P. The risk-reward for US equities is just not there.

NVIDIA will announce (stellar) earnings on Wednesday. Market reaction may not necessarily be stellar, as expectations are running dangerously high.

Dear reader, I have been wrong about the bond market. In April, I added to positions i my Beta (long-term portfolio). Rising agricultural commodities (ETF DBA) have helped, but not enough to offset a twenty-basis-point yield hit in my long-duration holdings. That translates to about a 2% loss in price.

A bond market saying comes floating back to my mind:

“Long and wrong.”

Although the momentum in the bond market is down, the beta portfolio is not for trading, and I am maintaining its current asset allocation.

Brazilian Markets

Brazilian local markets suffered a nasty double whammy. Globally, dollar strength knocked emerging market currencies down. Locally, the press revealed that conservative presidential candidate Flavio Bolsonaro maintained suspicious ties to the jailed owner of Banco Master, who has been accused of operating perhaps the biggest case of private/public corruption in Brazilian history.

Bolsonaro’s misfortune is President Luiz Ignácio de Lula’s windfall. The market shudders that the socialist Lula might win a fourth four-year term as President.

The Brazilian real devalued 3.21% to close at 5.05.

Editorial Note

There will be no feature post this Tuesday. I am reviewing the publishing schedule with the intention of achieving the most useful, inspirational, and enjoyable content possible.

I appreciate your support and understanding. If you have any feedback, please leave it on the website here.

The Macro Monitor

Bond market weakness and continued geopolitical stress outweigh positive earnings, giving the Macro Monitor a “risk-off” signal for the S&P this week.