A Spoonful of Sugar

I'm happy, hope you're happy too

“We have the best government money can buy.”

Mark Twain, 19th century American writer and humorist

Markets, like life, move fast. It seems to me like Covid had shut down the world just a fortnight ago, but it's been three full years since March 2020. In that time, we witnessed the Capitol overrun by hooligans, Kabul overrun by the Taliban, Ukraine overrun by Russians, and the economy and financial markets overrun with dollars.

The unwind started last year. Prices for everything and anything went up as supply chains were broken while economies were opening up, Proud Boys were jailed, Ukraine fought back, and the Fed lifted rates and started to remove some of the dollars it had dropped on the banking system, as former Fed Chairman Ben Bernanke, would say, “by helicopter.” Current Fed Chair Jay Powell began the work of tightening monetary policy with a better plan than Biden had to remove the United States from Afghanistan.

If there were such a thing as "everyday" people I would say that the gyrations of asset prices did not affect them through all this social, economic, political, and geopolitical upheaval.

What had gone up in 2020 and 2021, came down in 2022, and because we have the best government money can buy, happy days are here again.

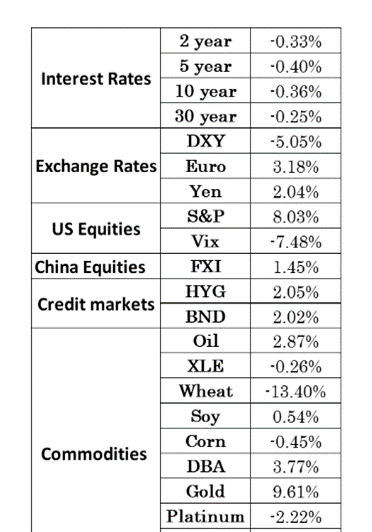

This is where we stand year to date.

We traders/analysts/investors are constantly searching for the right narrative to explain current market prices when of course, we should be searching for future market prices based on an expected narrative.

Retrofitting the market to the macro is relatively easy, although, for "everyday" people, the markets may seem to move randomly in shorter periods, but always move higher over decades. Owning some bonds to protect against lower equity returns during times of economic contraction smoothed out yearly volatility.

The narrative which explains the year-to-date performance of the main asset classes a macro fund manager trade – bonds, foreign exchange, stocks, and commodities – is two-fold.

The Weakening US Dollar

First, world trade has increased with the abrupt re-opening of the Chinese economy in late 2023 combined with the easing of commercial disruptions caused by the Russia-Ukraine war. Increased world trade is bearish for the US dollar.

Why? The United States has run a trade deficit with the rest of the world since 1994. It is a net exporter of capital and a net importer of goods and services. When world trade is bustling, or expected to bustle, the global system overflows with exported dollars, and the dollar goes down against other currencies.

The DXY Index is a composite of the Euro, the Yen, the Canadian Dollar, the British Pound, and the Australian dollar. That is the G-7 currencies.

The Covid-induced recession reduced world trade, and sparked goods and then service inflation, triggering sharp increases in interest rates.

This put the dollar on a solid upward trajectory until the third quarter of last year.

Since September, DXY has fallen an astounding 10%. Bad news for Americans hoping to travel to Europe on a string.

Dollars and other currencies are units in which goods are bartered. They are not goods themselves. Since 1973, the US Dollar is no longer guaranteed by gold reserves. It is only guaranteed by the "full faith and credit" of the United States. It is not the value of the dollar that changes, it is the value of the goods.

This is one of the most basic but not necessarily the most intuitive concepts in macroeconomics. Commodities traded internationally are priced almost exclusively in dollars. When marginal demand outstrips marginal supply for a commodity, holders of the commodity can charge more dollars for the same ton of iron ore or barrel of oil. The converse is that the same one-dollar bill buys a lesser quantity of that commodity than it did before. When commodities go up, the dollar goes down. Dollar devaluation is price inflation.

Each commodity has specific factors that alter its relationship to the US dollar. Oil jumped two weeks ago because of an unexpected OPEC+ production cut. Wheat has fallen 13% in 2023 as traders were relieved to see wheat production from Russia and Ukraine still flowing to global markets.

Three commodities stand out, and their appreciation is related to the falling dollar.

Although I am simplifying, China's re-opening has increased demand for these industrial products. Gold, a precious metal, is the other stand out, up 9.6% in 2023.

These commodities have not increased in price. Rather, the dollar has devalued against them. US equities are also denominated in US dollars. When there is downward pressure on the US dollar, that pressure acts to increase the value of US stocks relative to the dollar. The S&P is up 8% year to date.

The Fed’s Spoonful of Sugar

This leads us to the second part of the retrofitting macro narrative: The Fed. It's always the Fed, and it was its action last month when faced with the regional banking crisis that has underpinned the dollar weakness and the correlated commodity and equity strength.

I wrote in detail about the alien nature of Silicon Valley Bank and Credit Swisse bank run. "Life on Mars" referred not to the mismanagement and imprudence of these riverboat gambling banks, but rather to the panicked system-saving response of both the US Fed and the Swiss National Bank, with the obvious complicity of the US Treasury, the ECB, and most elected officials eager to avoid any type of prolonged economic distress that would make the financial system stronger and economic recovery more durable at the expense of potentially losing power.

Deposits outflows from the banking system into money market funds that purchase US Treasuries raise the cost of capital to the bank's customers – both retail clients looking to finance homes or cars – and corporate clients looking to finance new projects or refinance existing debt.

The market has reasoned that tightened credit conditions obviate the need for the Fed to raise rates higher than 5%. This weekend, for example, Secretary of Treasury Janet Yellen sweetly explained:

"Banks are likely to become somewhat more cautious in this environment," Yellen said in the interview, which is scheduled to air on Sunday. "We already saw some tightening of lending standards in the banking system before that episode, and there may be some more to come."

She said that would lead to a restriction in credit in the economy that "could be a substitute for further interest rate hikes that the Fed needs to make."

But Yellen said she was not yet seeing anything "dramatic enough or significant enough" in this area to alter her economic outlook.

"So, I think the outlook remains one for moderate growth and (a) continued strong labor market with inflation coming down," she said.

I have traded US interest rates since 1986 and emerging market interest rates since 1995. The volatility that we witnessed in March in the US interest rate market not only set American records but easily outmatched the volatility that often besets interest rates in emerging markets during crises.

Nevertheless, if you go back to the year-to-date table, across the yield curve, rates have moved insignificantly.

Today's US investor has again been saved by the Fed, for now. The common wisdom that inflation can be cured by economic recession has been challenged, even discarded, by the Fed, whose emergency extraterrestrial financing program avoided systemic stress in the banking system and its consequential economic fall-out.

As Paul Simon sings in his 1973 hit Kodachrome, “Everything looks better in black and white,” and this is where my retrofit ends and some colorful futurology begins.

The technical position of the S&P continues to be strong. Sentiment indicators continue to point to pessimism, indicating that the pain trade – the direction of prices that cause the most discomfort – is to the upside.

This is the S&P daily chart and its key technical indicator the 200-day moving average, explained here:

The bulls are in control. With the Fed's help, the market has shaken the negative consequences of the banking crisis and encouraged risk-taking. Bitcoin is flying once again, up 60% this year.

As Mary Poppins said, "A little bit of sugar helps the medicine go down."

My bearish option bets against the S&P have expired at a not insignificant loss, and I am not rolling them in deference of the technicals.

I’m happy earning 5% in the money markets, and tuned into the start of the first quarter earnings season and previews to the debt limit drama.