Mr. Bond and Mrs. Stock

Post-traumatic stress disorder

Post-traumatic stress disorder (PTSD) is a disorder that develops in some people who have experienced a shocking, scary, or dangerous event. It is natural to feel afraid during and after a traumatic situation. Fear triggers many split-second changes in the body to help defend against danger or to avoid it.

In 1961, the economist Milton Friedman theorized that monetary policy affects economic conditions only after a lag that is long and variable.

President of the Atlanta Fed Ralph Bostic echoed Friedman's postulate last November:

"Monetary policy unquestionably works with a lag. So, we at the FOMC calibrate policy today knowing we won't see its full impact on inflation for months. In those circumstances, we must look to economic signals other than inflation as guideposts along our path."

To bring inflation down from 10% to the Fed's objective of 2%, Chairman Jay Powell applied monetary shock treatment, raising interest rates from zero to five percent in fifteen months and ending its massive bond-buying program.

March's banking crisis that began with Silicon Valley Bank, pit-stopped at Signature Bank in New York, and continued across the Atlantic to Credit Suisse in Zurich, is the first serious lagged economic disorder we can attribute to the trauma of monetary tightening.

Before the Great Financial Crisis of 2007 and 2008, bank runs and failures were considered an evil but necessary part of a healthy economic system. Between 1980 and 1994, 1617 commercial and savings banks failed in the United States, the result of the Savings and Loans Crisis, another interest rate-driven trauma. Notwithstanding, from 1994 to 2007, the economy grew on average by 3.3% annually. After the epic government bailouts during the GFC from 2009 to 2019, growth averaged a skinny 1.80%.

Survival of the fittest once meant the extinction of the weakest. Creditors of a mismanaged bank, including depositors, took losses, but the system collectively became stronger. The stress brought on by the trauma dissipated over time.

Silicon Valley and Signature had been betting that interest rates would stay low enough to make a positive spread using overnight liabilities (customer deposits) to purchase government bonds of a longer duration. These bonds were labeled on the bank's balance sheet as assets "Held-to-maturity." When interest rates skyrocketed, the prices of these bonds fell. The banks were not required to recognize the loss and mark down equity on their balance sheets. This was perfectly legal.

Was it ethical? In my opinion, the losses were so large that the banks had a fiduciary responsibility to inform its stakeholders of the problem and communicate a plan to solve it. Instead, when deposits started leaving, the banks weres cornered into selling the bonds at market for a loss and and missed their chance to come clean.

When the remaining depositors got wind of the fire sale and smelled malfeasance, they withdrew their funds at an even faster rate, a rational reaction to the realization that the institutions had not been transparent. Both banks failed, but the remaining depositors, even those there were uninsured, were made whole by the FIDC.

Although the Fed purportedly understood that its interest rate shock would have "variable" impacts on the economy, obviously including stress on weak banks, within forty-eight hours of Silicon Valley's failure, it assumed its role as guardian of financial stability and rolled out a financing scheme to provide immediate liquidity to other banks that had committed the same sins.

Pope Powell's blanket pardon, called the Bank Term Financing Program (BTFP) not only allowed banks to continue to mismark their bond assets but allowed them to transfer those underwater bonds to the Fed and receive more cash than their market value.

The Wall Street Journal published an excellent article with a great title about the chicanery, “As Interest Rates Rose, Banks Did a Balance-Sheet Switcheroo.”

"At Wells Fargo, unrealized losses on held-to-maturity securities were $41.5 billion, equivalent to 23% of total equity. At U.S. Bancorp, they were $10.9 billion, or 21% of total equity. At Truist, they were $9.9 billion, or 16% of total equity. The percentages at JPMorgan and PNC were 13% and 11%, respectively."

Notwithstanding the Federal Reserve's acrobatics, PTSD is a chronic condition and the BFTP is a stop-gap measure. Even with the Fed's application of a palliative patch on systemic risk, Americans continue to wake up to the fact that it makes no sense to take the credit risk of the private sector – a bank – when the government itself pays them a higher rate.

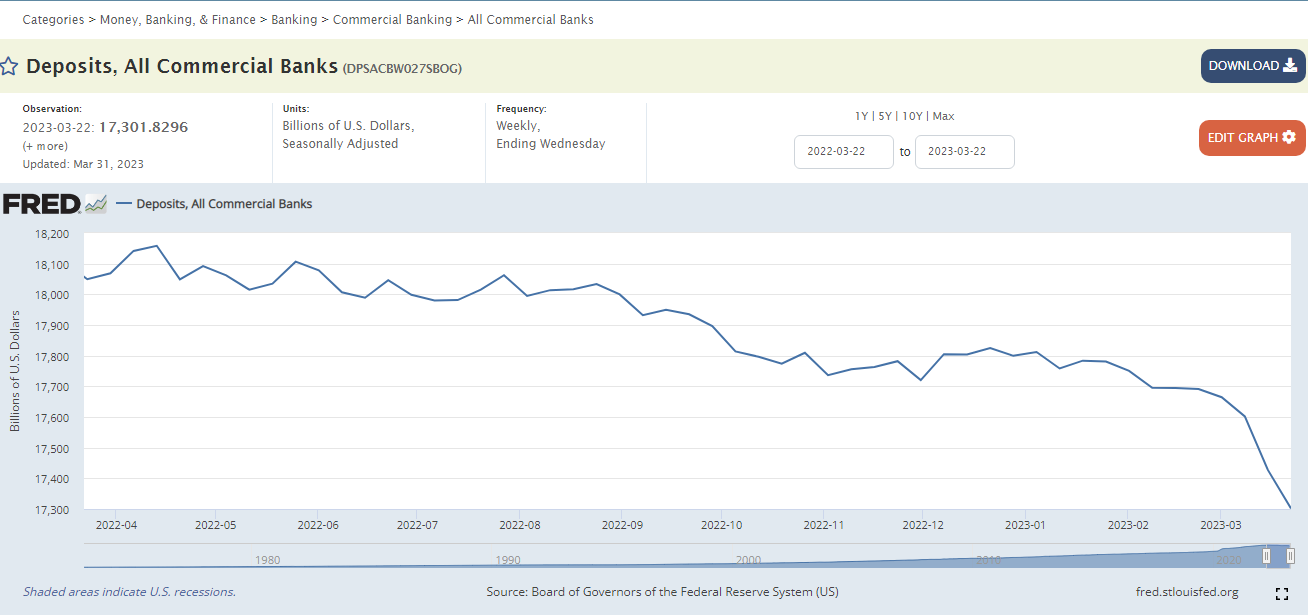

Look, for example, at the decline in bank deposits since the Fed began raising rates.

Until the first week of March of this year, the average weekly decline in deposits was $26 billion. In the second week of March, the outflow spiked to $98 billion, and in the third week, $53 billion.

In my last post “Life on Mars”, I wrote about the flow of these deposits into money market funds, and what this migration would do to the price of credit.

In the third week of March, money market assets increased by $126.7 billion, almost a mirror image of the deposit outflows. In the fourth week, the inflow was $61 billion.

Once in the money market fund, where does the money go?

The Vanguard Federal Money Market Fund is the largest money market fund in the country with $229 billion in assets. This is a snapshot of its holdings:

Repurchase Agreements make up the majority of the fund. In a "repo," as the transaction is known on Wall Street, the Fed sells a government bond from its portfolio to Vanguard with a promise to buy it back at a slightly higher price the next day. The difference in the two prices is the interest the Vanguard investor has earned on the transaction. Annualized, that investor is being currently paid 4.80% on an annual basis.

When I started life as a bond trader in the 1980s, only certain banks qualified as primary dealers could transact directly with the Federal Reserve. In 2014, as the Fed's creativity advanced, money market funds became eligible Fed counterparties. Today, money market funds have more than $2 TRILLION parked at the Fed.

The Fed has become ubiquitous. It effectively plays the role of the US Treasury in raising funds to finance the government, and it effectively plays the role of the private banking sector to safely hold and fairly remunerate deposits. It invokes trauma to control inflation and "destresses" its lagged consequences to guarantee financial stability.

The Atlantic Council published this excellent article on the subject, "Fed reverse repos hit a new record: An unhealthy development.”

In my March 13th post "The Macro Movie,” I compared the Fed to the Oscar-winning movie “Everything, everywhere, all at once.” I gave the New York Times permission to make the same comparison in another excellent article about the Fed's omnipresence.

And now, for a little entertainment and education, a parable about Mr. Bond and Mrs. Stock, and how they reacted to the stress of the March macro.

The Asset Family

(events based on a true story)

Mr. Stock and Mrs. Bond met in 2008 at an open house party that Mr. Bond's uncle threw for his neighbors. While it would be an exaggeration to say that they fell in love like in the movies, they indeed had a lot in common, and before long, they decided to wed and live life as a couple.

Year after year, they walked hand in hand. When it rained, Mr. Bond opened his umbrella, and neither he nor Mrs. Stock got wet. When Mr. Stock had a bad day, Mr. Bond was there to cheer things up, and vice versa.

Uncle Bond always threw a lavish party at New Year's. It became their tradition to commemorate by toasting with Dom Perignon and nibbling on petit fours.

Both of them, we could say, were fulfilled assets.

That was until 2022 when Mr. Bond's uncle passed away suddenly, and the marriage began to fall apart. Mr. Bond fell into a deep depression and instead of fulfilling her wifely duty to cheer him up, Mrs. Stock fell into her own rut. As 2023 started, they seriously considered divorce.

On March 10th, Mr. Bond and Mrs. Stock were watching their favorite TV show, Mad Money, when they heard Jim Cramer say, "banking crisis." That was enough for Mr. Bond to put on his sweatpants and run frantic laps around and around the block. Mrs. Stock was so surprised by Mr. Bond's reaction, she fell off the couch.

During the last week of March, Mr. Bond finally ran out of gas and fell asleep on the couch.

When he woke up, he told Mrs. Stock, "Dear, I dreamed that my uncle has come back to life."

Mrs. Stock clapped her hands. What was good for the goose would be good for the gander! Lavish parties would be back. They would renew their wedding vows!

She decided she would follow Mr. Bond and put in her own run around the block.

The End

Cast of Characters

Mr. Bond: The United States Bond Market

Mrs. Stock: The Composite S&P 500 Stock index

Mr. Bond's rich uncle: Quantitative Easing, the Federal Reserve's bond-buying program that ended in 2022.

The marriage: The traditional investor portfolio composed of 60% stocks and 40% bonds.

Mr. Bond's frantic laps around the block: The bond's markets neurotic fear of an economic hard landing, with two-year treasuries falling from roughly 5% to 4% in March and Long Treasuries rising 6 points.

Mrs. Stock's end-of-the-month conversion: The S&P's stellar and schizophrenic comeback, closing 2% higher than its close before the crisis started.

The moral of the story: A wife will do what she wants, regardless of what her husband says.

(If you liked this content, please leave a like and suscribe! It’s free)

A year-by-year history of the Asset Family