What a Relief Rally

Macro Monitor, April 19, 2026

Last Week

What is a relief rally?

A relief rally is a short-term, often sharp increase in stock prices (or other asset prices) that occurs after a period of significant decline or market selloff. It provides investors with a temporary “sense of relief” from falling markets, but it does not necessarily signal the end of the broader downtrend. (Investopedia.com)

Falling markets often experience relief rallies. But last week, what a relief rally!

The week began with the failure of peace talks in Islamabad. Markets traded sharply lower on Sunday night, but by Monday morning, the S&P was unchanged.

By the end of the week, the S&P had rallied 4.5% and the Nasdaq 6.2%. In fact, Friday was the thirteenth consecutive positive day for both indices.

Markets believe what they want to believe. This week, markets put faith that President Trump’s shift from military coercion to economic coercion could pressure the regime into concessions. Markets were encouraged by Trump’s repeated affirmations that a deal was near, that negotiations would continue, and that the US would be able to take possession of Iran’s enriched nuclear “dust.” (Trump calls it “dust” because he maintains it was buried deep in the ground by the B-52’s that bombed Iran last May.)

Adding fuel to the rally, the money-center banks reported strong earnings and a sanguine economic outlook.

Oil traders were also relieved, with front-month WTI futures falling 8%. December 2026 futures were less impressed with the newsflow, falling just 3.5%.

There was little joy in Treasuries. Although two-year yields mechanically fell ten basis points alongside oil prices, the long end of the market could not keep pace with the risk-on environment. The thirty-year Treasury yield fell just 2 bps to 4.91%.

The S&P is now higher than it was before the outset of the war. Higher by 3.5%. By contrast, longer-duration bonds are down about 1% in price, with yields up about 15 basis points.

That is a divergence that makes the relief rally suspect.

Bonds appear cheap to stocks. This was the subject of last month’s post, “The Contrarian Trade of 2026,” which argues in favor of owning much-hated Treasuries.

This thesis has not yet materialized in the markets. That is not unusual. To time a reversal of an unloved asset class is almost impossible. Patience is necessary.

The Coming Week

Over the weekend, Iran turned up the hostilities meter and pronounced the Strait closed again. The US is preparing to board Iranian vessels in the Gulf of Oman. There are reports that Iran has attacked commercial ships.

The ten-day ceasefire is scheduled to end on Wednesday. Expect competing bull and bear headlines to determine short-term price action.

Keep an eye on those Treasuries. If they continue to trade poorly, it will be difficult for the S&P to add another leg to its relief rally.

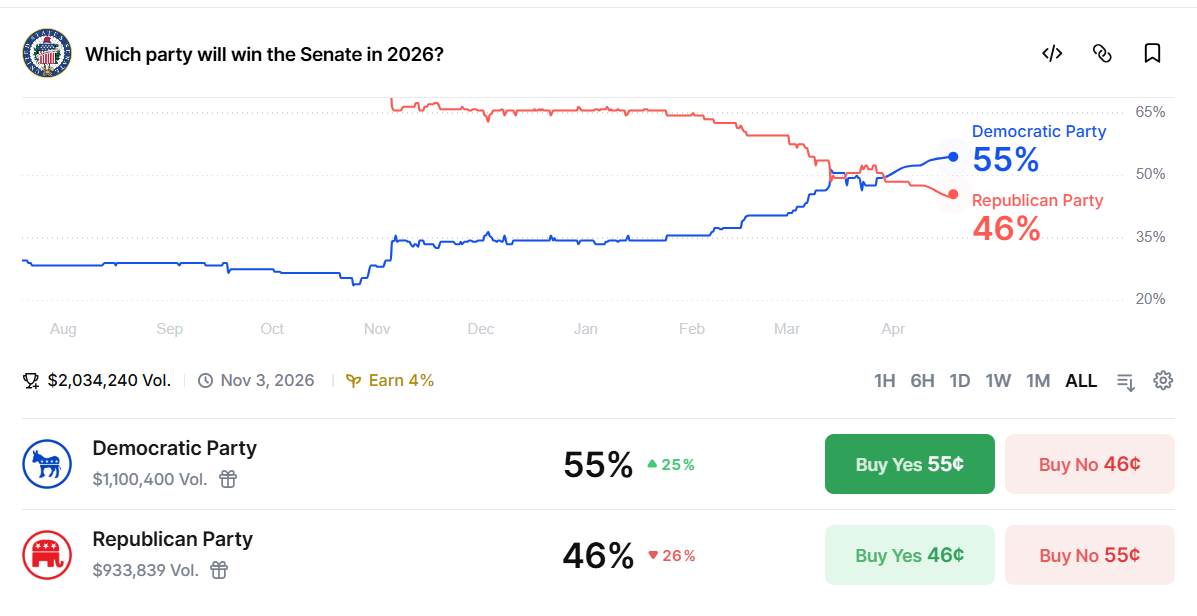

Also worth noting is an important shift in the betting markets.

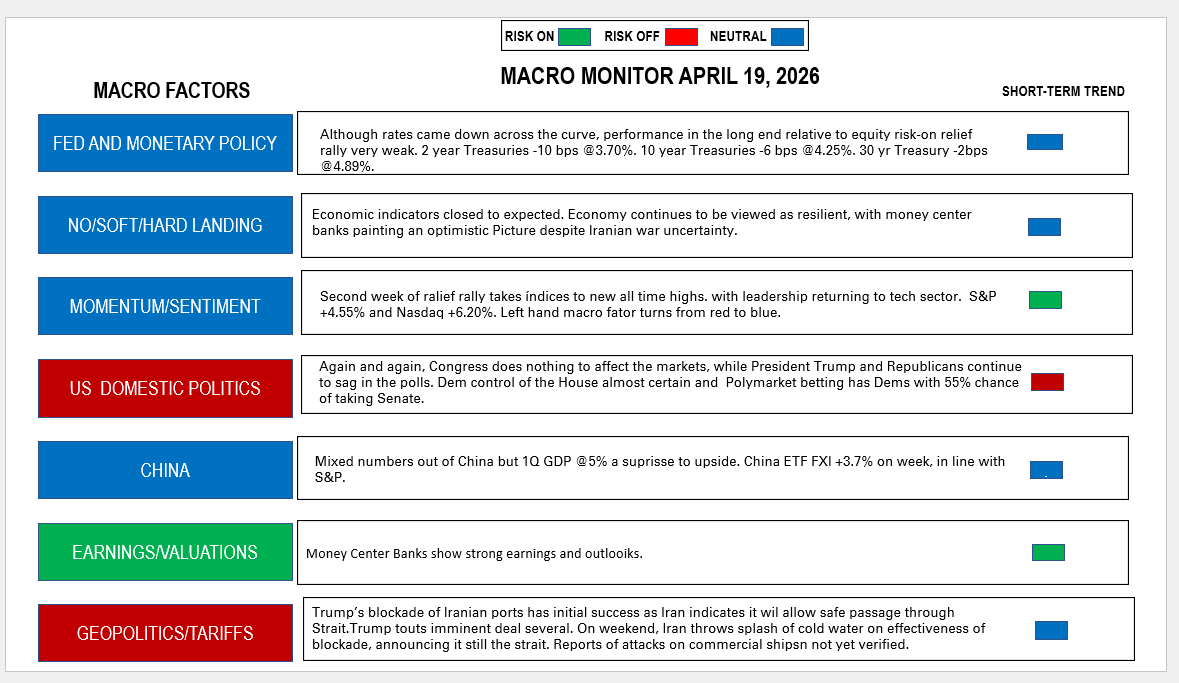

Over the last month, the Democrats have become favorites to win the Senate in November.

This is the Polymarket chart showing the recent crossover:

What would the market impact of the Democrats winning back both the House and the Senate be?

In general, markets “prefer” Republican government to Democratic government. When Trump won the Presidency, for example, the S&P rallied 5% in twenty-four hours.

This time around, it is more difficult to say Republicans are “good” for the markets and Democrats “bad.” Both parties have shown a disregard for fiscal discipline, and Trump is a unique president who does not fit the traditional Republican mold.

Markets may embrace the gridlock of divided government or may fear the potential political instability of a Democratic Congress squaring off against a lame duck Trump administration.

Domestic politics will soon be joining geopolitics as a market mover.

Brazil

The Brazilian real traded below 5 for the first time in two years.

Despite this landmark, Brazilian assets did not keep up with the S&P. The Brazilian ETF EWZ rose 1.50%.

The Macro Monitor

The Monitor got it wrong, again, last week, predicting a risk-off environment ahead of a week of epic rally.

Dear reader, remember: “To err is human, to forgive, divine.”

Forgive me!

This week, based on the breakout to new highs, the macro factor “Momentum/Sentiment” shifts from red to blue. With this change, the reading for the coming week is exactly neutral.

Note: I am lucky enough to be visiting my dear mother in Alexandria, Virginia, this week. For that reason, I will not be publishing the regular Tuesday feature.

If you agree that Mrs. Wolf is more important, then give this post a like!

Thanks, David

Enjoy the trip! Mrs Wolf is definitely more important!!!