Resilience and Resistance

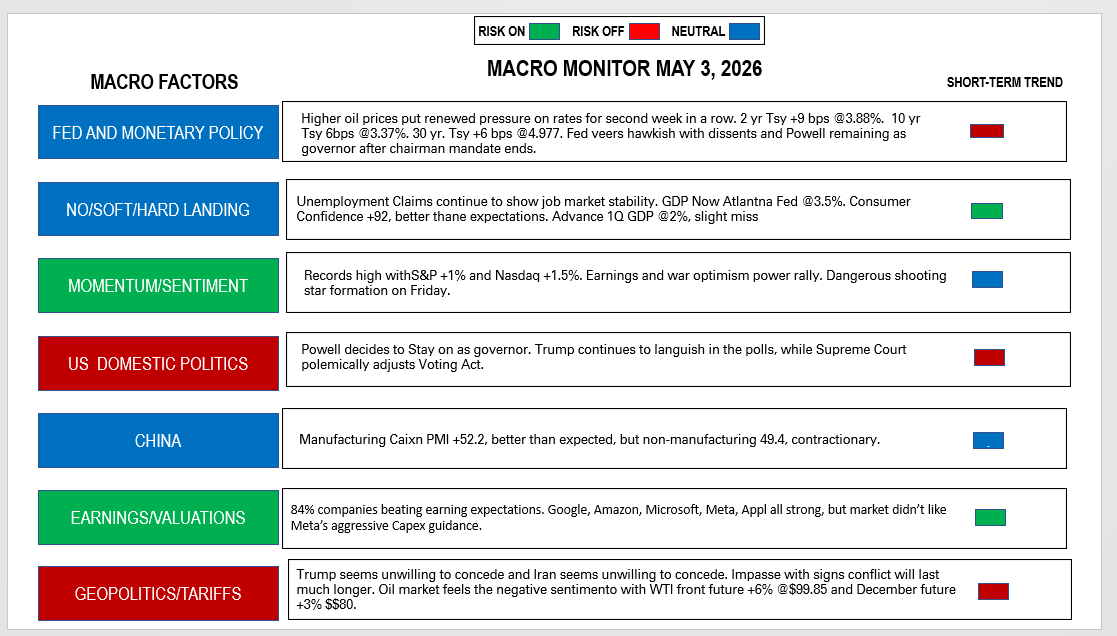

Macro Monitor, May 3, 2026

Last Week

To understand what drove markets last week, let’s take a look at the Macro Monitor. There were developments in six of the seven long-term Macro Factors on the left.

[For those of you who don’t follow the Monitor weekly, the “instructions” on how to interpret it are at the end of this post.]

The Fed

Interest rates moved higher in tandem with oil, which rose 6%. The two-year treasury rose nine basis points to 3.90%. That puts it 25 basis points over the overnight federal funds rate, a general indication that markets anticipate the next move by the Fed will be a hike.

The Fed left interest rates unchanged on Wednesday, but its bias was hawkish. Three board members officially registered that they disagreed with the sentence in the Fed’s statement that indicates likely future rate cuts.

At Jerome Powell’s last press conference as Fed Chairman, he said inflation was “moving in the wrong direction.” In fact, with oil prices rising and beginning to contaminate the price of agricultural commodities, the risk is that the CPI, which in reported at 3.3% in March, touches 4% before 2%. in the next six months.

Kevin Warsh will assume the chairmanship of the Fed later this month. He will not only have to confront these inflationary pressures, but also will face the continued presence of Powell on the board. Citing Trump’s lawsuits aimed at him and the Fed as politically motivated and dangerous to Fed independence, Powell announced he has opted to remain a voting member until his term as Governor (not-Chairman) expires in January 2028.

Although traditionally dovish, Powell may continue to be a thorn in Trump’s side and resist any attempt by Warsh to lower interest rates if the data do not support cuts.

The Economy

Unemployment claims registered 187,000, the lowest reading since 2023. The economic data support the narrative that the economy is showing remarkable resilience in the face of geopolitical uncertainty and gloomy consumer sentiment surveys.

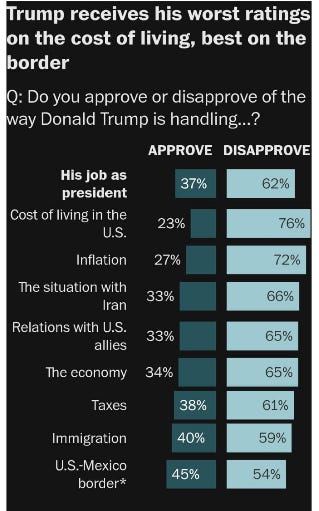

Domestic Politics

President Trump continues to suffer in national polls. These are the results of the Ipsos poll taken in the last week of April.

Markets have not yet begun to price in the growing probability that the Democrats may regain control of both houses of Congress in November.

Momentum/Sentiment

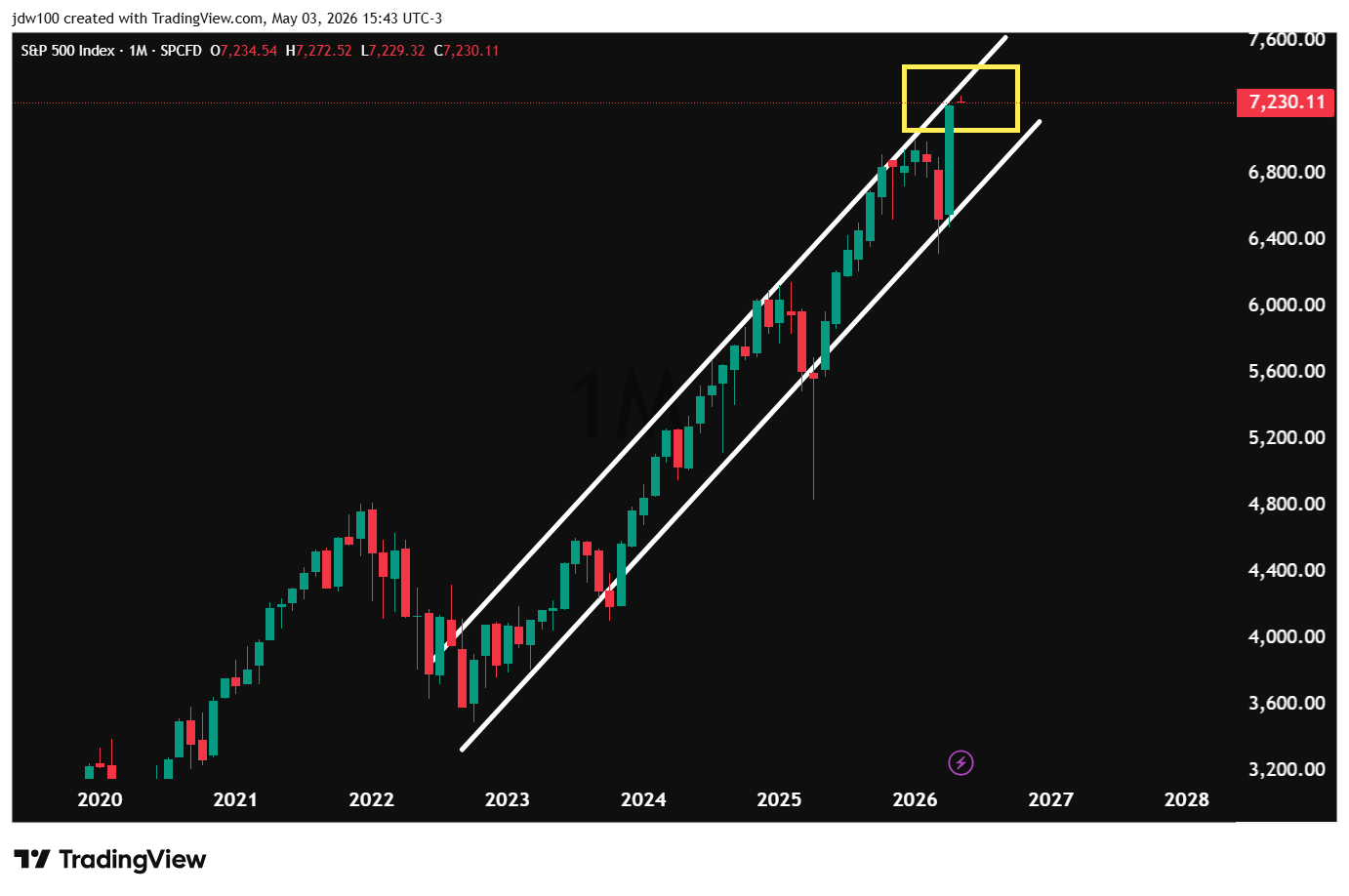

Both the Nasdaq and the S&P rose by more than 1%, once again setting all-time highs. One disconcerting technical signal is the “shooting star” formed on the S&P daily chart on Friday, where the market closed where it opened after a strong intraday rally failed.

If this technical formation is confirmed by lower prices on Monday, the market may have put in a near-term top.

On the monthly chart, the SPX (S&P cash) is pushing against strong resistance on the long-term bullish channel initiated in 2022.

Earnings

One of the inherent features of the Macro Model that limits its predictive power is that markets never put equal weight on each macro factor. Sometimes, monetary policy influences prices more than geopolitics. Sometimes sentiment overrides earnings.

In the present market context, earnings have been the most impactful market driver.

The S&P has rallied 10% from its March low, powered not only by the expectation that the Iran war will be resolved quickly, but that corporate profits will continue to grow in the neighborhood of 20% in 2026.

Financial giant Visa is well-positioned to evaluate trends in the broader economy.

This is an excerpt from CFO Chris Suh's comments on the investor call:

“U.S. payments volume grew 8% year-over-year, up almost 1.5 points from Q1, reflecting resilience in consumer spending…Across our volume, both discretionary and nondiscretionary spend remains strong. We do not see signs of the lower spend consumer weakening in our volumes.”

Equity markets, like consumers, are ignoring higher energy prices. The bulls, who are putting corporate earnings and economic strength over inflationary pressure and Fed hawkishness, are winning the battle.

Geopolitics

The war is at an impasse. Ideally, Trump would declare victory and end the war. That isn’t possible as long as the Strait of Hormuz remains closed. He appears to be working on a deal to end the US blockade of Iranian ports in exchange for Iran reopening the Strait. That would be positive for markets, but would imply leaving the regime with tons of enriched uranium. But that would mean that Trump would leave Iran with tons of nuclear material and the ability to resume its development of nuclear weapons. That is an unpalatable resolution for the President.

An impasse indicates energy, fertilizer, and food prices will stay higher for longer.

This is what Exxon Chairman and CEO Darren Woods said on CNBC on Friday

“It’s obvious to most that if you look at the unprecedented disruption in the world supply of oil and natural gas, the market hasn’t seen the full impact of that yet… There’s more to come if the strait remains closed.”

He makes two other interesting observations:

Demand is currently being met with supply that existed before the war - on the water and in storage facilities. Countries have also made available strategic reserves to soften the blow. As time passes, that supply is consumed, creating upward pressure on prices.

When transit returns to the Strait, governments will have to rebuild those depleted strategic reserves, putting pressure on prices down the road.

Chevron CEO Mike Wirth made similar comments on “Face the Nation” today (Sunday).

The Coming Week

The economic calendar may take center stage over earnings. Two of the most important monthly indicators will be released.

On Wednesday, April ISM services is expected to print 53.

On Friday, the April non-farm employment component of the employment report is expected to show 60,000 jobs added.

The wildcard will be the Treasury’s Quarter Refunding Announcement (QRA), released in two parts - on Tuesday and Wednesday.

Simplifying a complex subject, the Treasury informs the market of its borrowing needs for the present quarter and guidance for the next, announcing the expected size of Treasury bill, note, and bond auctions.

Markets expect the supply of longer-term bonds (duration) to stay unchanged. There is an outside chance that Secretary Bessent might reduce duration and thereby “juice” both financial markets and economic growth with artificially long-term interest rates.

The effect of such a move toward financial repression, however unlikely, would be significantly higher asset prices (especially gold) and a crashing dollar.

The Macro Monitor monitors market conditions to present an easy-to-visualize and objective summary of the previous week’s price action and relevant macroeconomic changes.

Just eyeball the Monitor for this week at the beginning of the post, and it is fairly clear that the signal is close to neutral.

Subjectively, I believe that the risk-reward has become skewed to the downside. The rally has met technical and geopolitical resistance that may finally test the market’s recent resilience.

In my alpha (trading) portfolio, I bought 4% out of the money puts on the S&P with July expiration and put spreads a little further out of the money.

In the beta (long-term) portfolio, the only change was to increase the gold position.

Please leave a like here if the Macro Monitor has indeed helped you analyze the markets.

Thanks, and have a good week.

Tuesday Teaser

Tuesday’s feature will analyze why the market gods have favored equities over bonds, using esoteric references to medieval romanticism and modern nihilism to make the point as clear as possible.

Macro Monitor “Instructions”