In War, Truth is the First Casualty

Macro Monitor, April 5, 2026

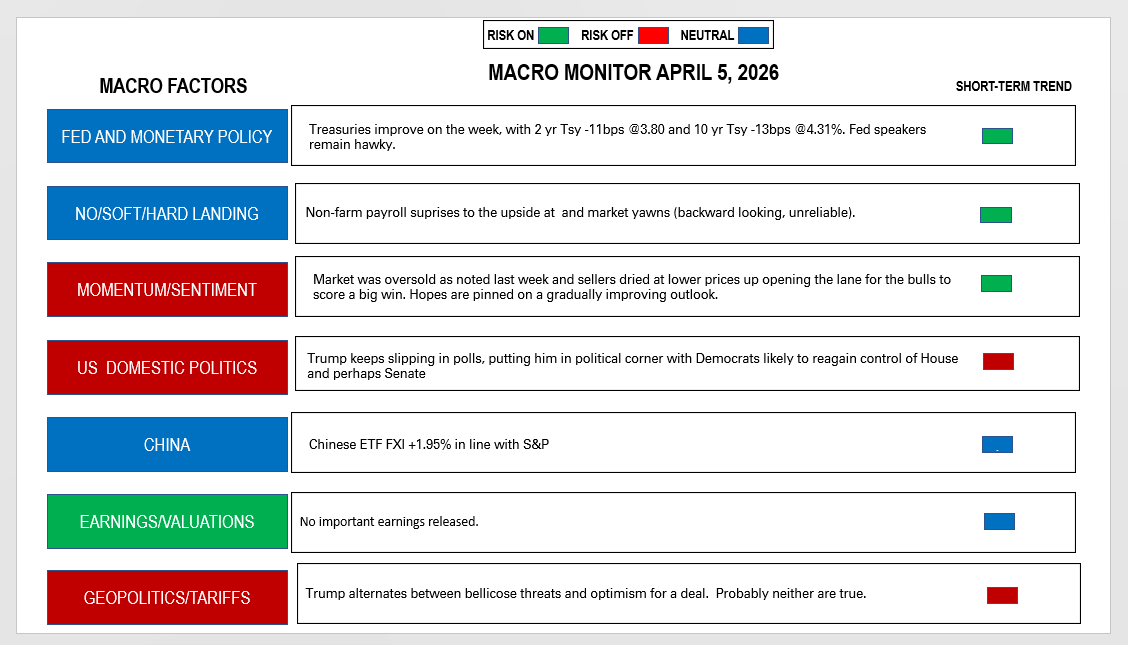

Last Week

According to legend, the Greek playwright Aeschylus met a tragic death: one day, an eagle that had just caught a tortoise mistook Aeschylus's bald head for a shiny rock and accidentally killed him by dropping the tortoise on it. Evidently, the eagle was hungry for turtle meat and thought he could break its shell by dropping it on the poor dramatist’s shiny cranium.

That parable could describe the state of today’s markets, where logic and truth have been made to stand on their heads.

Aeschylus was also a military hero, a veteran of the Greco-Persian War that pitted a fractured Greek empire against the mighty Persian empire. Persia, of course, is the historic region of southwestern Asia associated with the area that is now modern Iran.

At the Battle of Marathon in 490 BC, the Greeks, against all odds, repelled the Persians. The hero Philippides ran twenty-six miles to report to Athens’ leaders:

“Rejoice, we conquer,” Phillippides said, before collapsing and dying.

So was born the long-distance race we now know as the marathon.

Aeschylus himself also coined this eternal phrase:

“In war, truth is the first casualty.”

Truth has never been as elusive as it is in today’s geopolitics. Consider these competing narratives:

Iran was close to a nuclear weapon and posed an imminent threat; there was no such threat - Trump was manipulated by Netanyahu.

America will blow Iran back to the Stone Age; the regime is begging for a deal.

The Strait of Hormuz is closed to all traffic; some tankers are paying a toll and sailing through.

The Iranians are out of missiles and drones; missiles and drones continue to wreak hit the Gulf States, and three American fighter jets are shot down.

The left-wing press calls Trump’s “excursion” the most misguided military action of all time; The right-wing press heralds the domination of Iran by the US military.

The contradictions extend to the financial markets.

Oil closed at virtually the same price on March 27 as on March 13. But during those two weeks, the 10-year Treasury yield screeched higher, from 4.28% to 4.44%, while the S&P sunk 3.5%.

Last week, oil was the mover, up 6%, but both Treasuries and stocks ignored it. The ten-year dropped ten basis points to 4.31%, and the S&P rose 3.26%.

The truth about the state of the economy is also elusive. On Friday, the Bureau of Labor Statistics reported a huge 178,000 jump in nonfarm payrolls in March, compared to a decline of 133,000 in February.

Go figure.

The Coming Week

Will President Trump announce boots on the ground - 500, 1,000, 5,000 - charged with taking control of the Strait of Hormuz, commandeering the oil installations on the island of Kharg, or hunting down Iran’s enriched uranium?

Or will he declare victory and take the American forces home? Leave the bombing of Iran for Israel, and opening up the Strait of Hormuz for the Europeans and the Asians?

Or will he do both?

The best bet is that the week will end without answers to these questions and Aeschylus will have the last laugh.

For what it is worth, we will get more economic data points - ISM Services, CPI, and PCE - which during peacetime would carry weighty significance. War will probably overshadow these releases, but if, as a whole, they show economic strength and inflationary pressures, risk assets will suffer as that puts Central Banks around the world further away from monetary easing.

Brazil

The currency appreciated 1.8% in line with better global risk appetite and closed at 5.15. The Brazilian ETF EWZ appreciated 5%.

The Macro Monitor

The Monitor got it wrong last week, forecasting “risk-off” for the S&P. The model often errs in extremely overbought or oversold conditions, and last week’s S&P snapback was more a result of poor positioning by the bears than heightened geopolitical or macroeconomic clarity.

This week, the signal is a very slight “risk-off.”

Best advice: Leave core positions alone. Don’t overtrade. Pray.